Key headlines from January - Offtakes pass $10Bn mark in 2025, EU carbon farming rules and nature-based deals

Monthly newsletter on news from the New Forest Economy

Welcome to Arbonics’ monthly roundup of news relevant to forests, the voluntary carbon markets, and climate solutions more broadly. Bringing you the latest that catches our eye - as well as our own take on the news.

January is traditionally the month when the big annual reports land, and 2026 is no exception. We are seeing a market in transition: while spot volumes remain steady, the massive growth in forward offtakes suggests a structural shift toward long-term, high-integrity partnerships. This month, we’re diving into the latest market data and “hot off the press” news on EU’s own certification scheme for voluntary carbon credits.

Data backing up the move to VCM 2.0 from both Sylvera and Allied Offsets

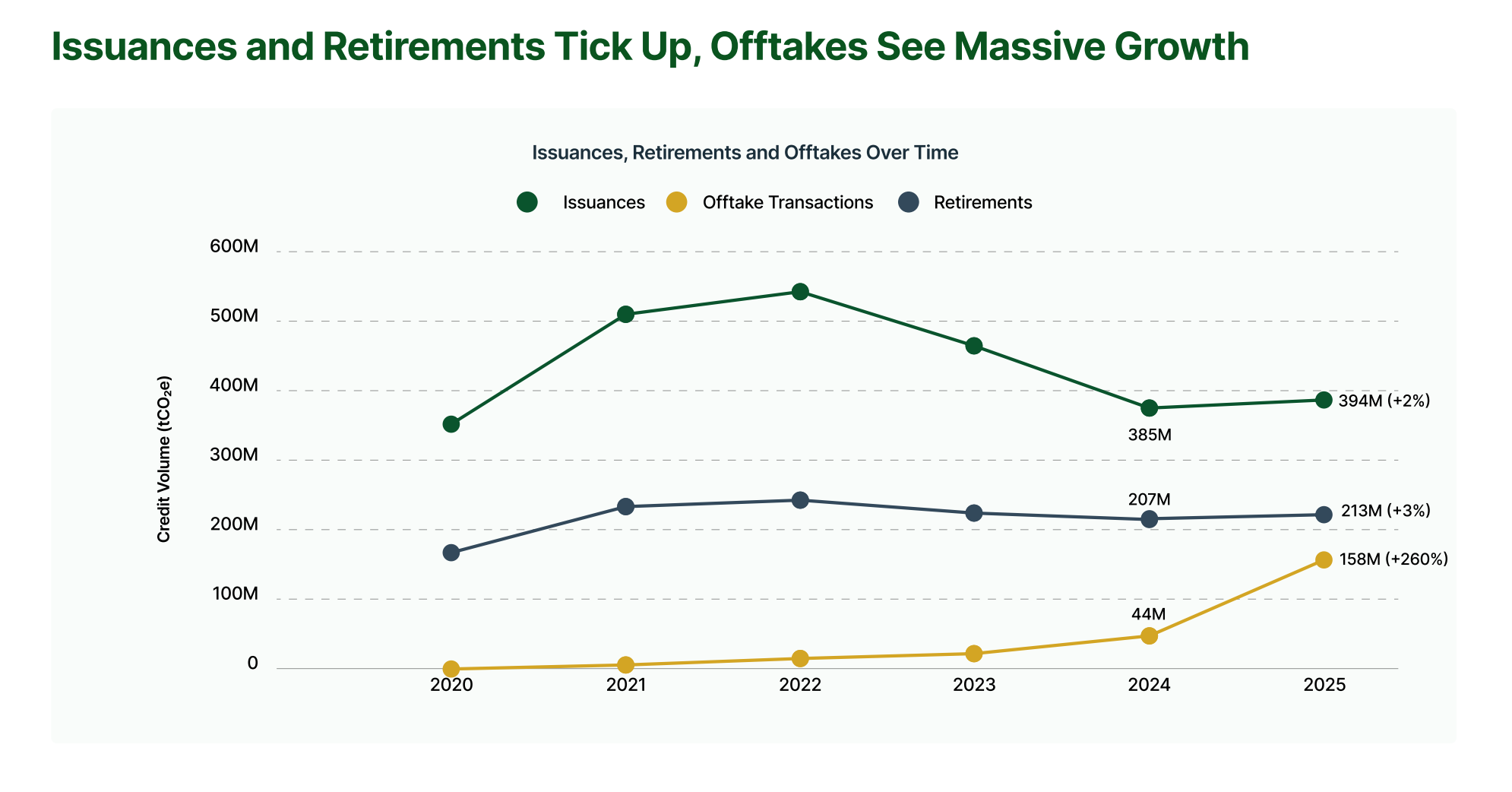

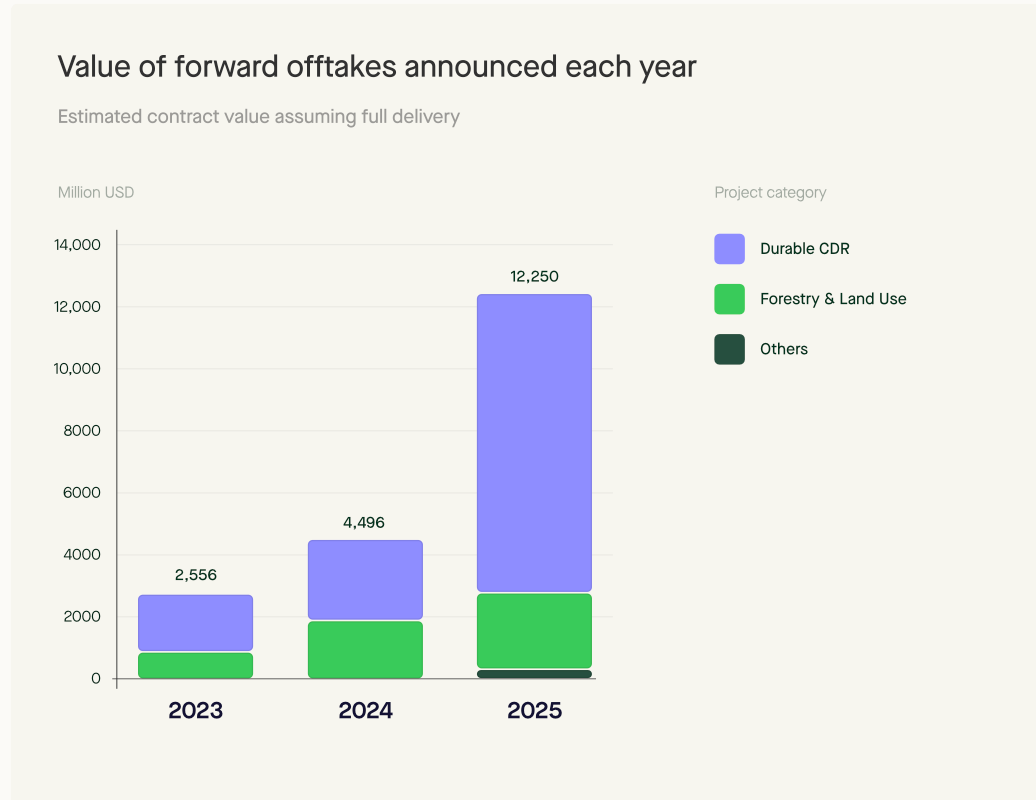

If you are a long time reader, you might remember Kristjan’s article on the move from voluntary carbon market v1 (VCM 1.0) to VCM 2.0. Don’t just take our word for it, two big players in the space, Sylvera, a credit ratings agency, and Allied Offsets, a market intelligence platform, have just released their reports with the latest 2025 data and it’s clear: offtakes are taking off.

Both reports reveal that carbon market is shifting from “volume to value”. While the number of unique buyers has stayed relatively flat at around 8,000, the total value of offtake agreements announced in 2025 has surpassed $10 billion. Sylvera reports, that there is a concentration of forward deals among a small cohort of roughly 100-200 sophisticated buyers who are increasingly willing to pay a premium for quality, with average offtake prices for removals hitting $160 per tonne.

💡 Arbonics’ take:

The “flight to quality” is now a reality. High-integrity projects are increasingly decoupled from the low-priced spot market, as buyers secure future supply to meet 2030 targets.

EU delivers first methodologies as part of CRCF and opens public consultation on carbon farming

The EU has adopted the first voluntary methodologies for permanent removals (DACCS and Biochar) as a benchmark for the Carbon Removals and Carbon Farming (CRCF) framework.

The European Commission has opened a public consultation on draft certification rules for carbon farming, which includes activities such as afforestation, peatland rewetting, and agroforestry. These rules aim to harmonise how carbon farming is certified across the EU, ensuring transparency, additionality, and robust monitoring to build trust in European voluntary markets. The process invites input from companies, land managers and wider stakeholders on how carbon farming should be certified and governed across the EU. Feedback is open until 19 February, and will directly inform the final rules that underpin Europe’s voluntary carbon farming system.

💡 Arbonics’ take:

Seeing the publishing of first methodologies is a huge milestones for the market and we have been waiting for it since CRCF was announced by the European Commission in November 2022. The framework establishes EU-specific rules for carbon removal certification that will run parallel to (not replace) existing voluntary market standards like Verra’s Verified Carbon Standard. Clear standards are exactly what European landowners and investors need to scale up projects. We are providing feedback and following the process closely.

A good first month of the year for NbS across the spectrum: soil, forestry and biomass burial

Microsoft continues to dominate the removals space. In January, the tech giant signed a record-breaking 12-year deal with Indigo Ag for 2.85 million soil carbon credits. This was closely followed by a 2-million-tonne afforestation offtake via Rubicon Carbon from the Kijani Forestry project in Uganda, which supports over 50,000 smallholder farmers. Finally, Mast Reforestation delivered the first-ever credits from its biomass burial and post-fire restoration project in Montana. They buried over 10 million pounds of wildfire-killed biomass, securing it for at least 100 years.

💡 Arbonics’ take:

These deals highlight the diversity of high-quality nature-based solutions (NbS) but also that NbS continues to be a popular choice to provide volume of credits, while technical removal supply is slow to pick up. In addition to the volume of carbon credits these solutions deliver, they also come with many social and ecological co-benefits, whether it’s restoring fire-damaged forests or working with smallholders in Uganda.

Thanks for reading! Let us know what you think by replying to this email (or hello@arbonics.com).